What is a Home Appraisal?

Whether you’re buying, selling, or refinancing a home, a crucial step in the process is understanding what is a home appraisal and how it impacts your financial decisions. A home appraisal is an unbiased professional evaluation of a property’s value, typically required by lenders when a mortgage is involved. Knowing what a home appraisal consists of and what factors influence it can help you understand the transaction confidently.

The Home Appraisal Process and Cost

The home appraisal process begins when a licensed appraiser is hired—usually by the lender—to assess the property. The appraiser’s job is to determine the home’s market value, ensuring that the property is worth the amount being borrowed. This evaluation helps protect the lender by preventing over-lending, which could lead to financial losses in case of default.

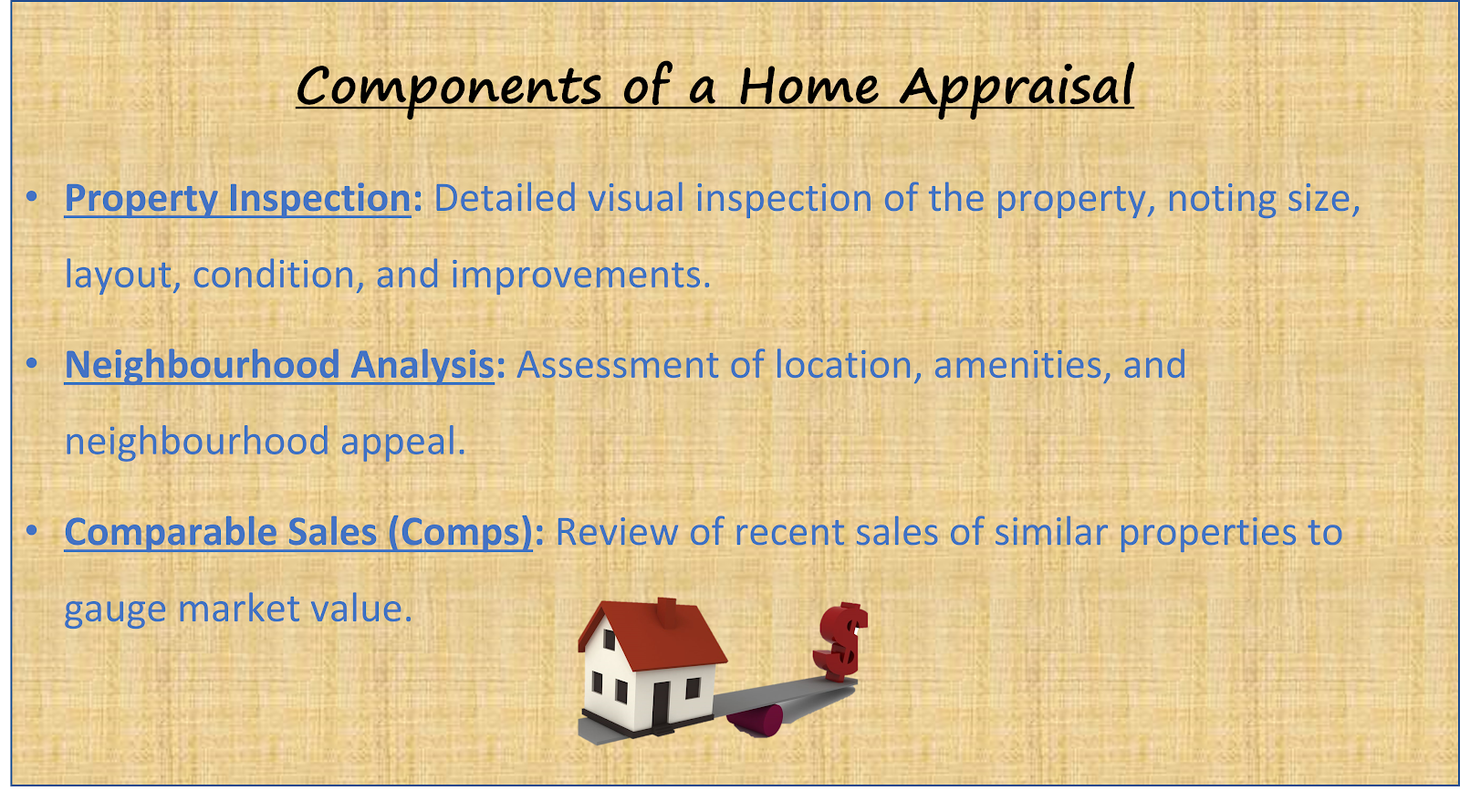

Components of a Home Appraisal:

- Property Inspection: The appraiser conducts a detailed visual inspection of the property, both inside and out. They note the size, layout, condition, and any improvements made to the home.

- Neighbourhood Analysis: The surrounding area plays a significant role. The appraiser considers the home’s location, proximity to amenities, and overall appeal of the neighbourhood.

- Comparable Sales (Comps): The appraiser reviews recent sales of similar properties in the area, known as comparables or “comps.” These help determine the home’s value based on market trends.

Cost of a Home Appraisal:

The cost of a home appraisal is typically around INR 3500. The price varies depending on factors such as the size of the home, its location, and the complexity of the property. Larger or more complex properties require more time and research, resulting in higher costs.

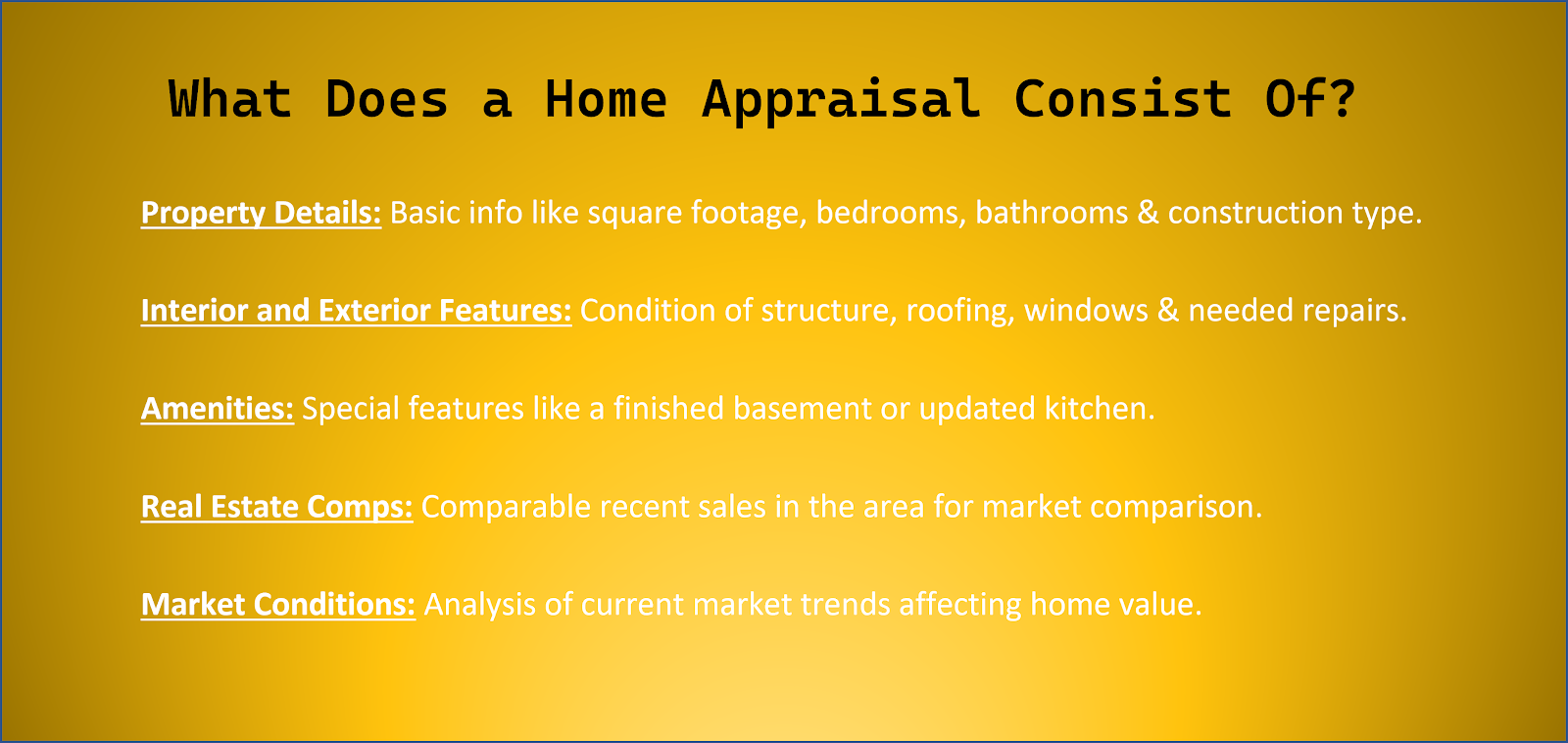

What Does a Home Appraisal Consist Of?

Understanding what a home appraisal consists of is key to anticipating the outcome. A typical appraisal report includes:

- Property Details: Basic information such as square footage, the number of bedrooms and bathrooms, and the type of construction.

- Interior and Exterior Features: Details about the home’s condition, including structural integrity, roofing, windows, and any noticeable repairs needed.

- Amenities: Any special features like a finished basement, swimming pool, or updated kitchen can increase the property’s value.

- Real Estate Comps: The report contains information about comparable properties in the area that have recently sold, allowing for an objective market comparison.

- Market Conditions: Current market trends and conditions affecting the home’s value are analysed to ensure an accurate appraisal.

What Homebuyers Need to Know About Home Appraisals

For buyers, an appraisal can be a decisive factor in the transaction. If you’re buying a house with a mortgage, the lender uses the appraisal to confirm that the property’s value justifies the loan amount. If the appraisal comes in lower than the agreed-upon purchase price, you may need to renegotiate with the seller, provide a larger down payment, or even walk away from the deal if the gap is too large.

Buyers should also be aware of potential issues that could affect the appraisal, such as outdated or damaged features, which might lead to a lower valuation. In some cases, buyers have the option to dispute the appraisal if they believe it was inaccurately done.

Read More: Best Home-Buying Checklist for a Smooth Home-Buying Experience!

How Much Does a Home Appraisal Cost?

The appraisal cost, as mentioned, is typically around INR 3500. Several factors influence this pricing:

- Size and Complexity of the Home: Larger properties or homes with unique features often require more time to appraise.

- Location: Homes in rural areas may incur higher costs due to the appraiser’s travel and the scarcity of comparable sales.

- Type of Appraisal: Hybrid or desktop appraisals, which involve fewer in-person visits, may be cheaper than traditional methods.

Who pays for the appraisal? In most cases, the buyer is responsible for this cost unless negotiated otherwise. However, understanding what is a home appraisal and how much it costs gives you a better sense of the financial obligations involved in the home-buying process.

How Long Does a Home Appraisal Take?

The timeline for completing an appraisal varies but typically ranges from several days to a few weeks. The inspection itself can take anywhere from 15 minutes to a few hours, depending on the size and condition of the property. Following the inspection, the appraiser analyses market data, evaluates comparables, and prepares the final report, which is then sent to the lender.

What Happens After the Appraisal?

Once the appraisal is complete, the lender reviews the report to ensure it aligns with the loan application. If the appraisal meets or exceeds the purchase price, the transaction moves forward as planned. However, if the appraisal comes in low, the deal may need to be renegotiated, or the buyer could be required to pay the difference out of pocket.

In a refinancing scenario, the appraisal determines how much equity is available in your home. A higher appraisal can unlock better loan terms, while a low appraisal might limit your options.

Read More: Latest RBI Guidelines for Home Loans 2024

Conclusion

A home appraisal is an essential step in real estate transactions. For those looking to manage this process smoothly, PropertyPistol provides end-to-end real estate services, ensuring that your property journey is seamless and hassle-free. Whether you’re buying, selling, or refinancing, knowing what is a home appraisal and what does a home appraisal consists of can help you understand the process with confidence. By understanding the factors that influence the appraisal, you can better prepare yourself and avoid potential roadblocks in your real estate journey.

FAQs

Do I need to get a home appraisal?

Yes, if you’re purchasing a home with a mortgage or refinancing, your lender will likely require a home appraisal. Even if you’re paying in cash, getting an appraisal is still recommended to ensure you’re paying a fair price.

Who pays for the home appraisal?

Typically, the buyer pays for the appraisal as part of the closing costs. However, this can sometimes be negotiated during the purchase agreement process.

What can I do if I receive a low appraisal?

If you receive a low appraisal, you have options. You can request a review or appeal, providing additional evidence like more appropriate comparable sales. Alternatively, you can renegotiate the price with the seller or bring extra cash to cover the difference.

Disclaimer: The views expressed above are for informational purposes only based on industry reports and related news stories. PropertyPistol does not guarantee the accuracy, completeness, or reliability of the information and shall not be held responsible for any action taken based on the published information.